ລາວ

ລາວ

{kind=link}

Core Grade A Offices Lead Rental Recovery, Hong Kong Island High Streets Outperform Kowloon

- Residential Market: Q2 residential transaction numbers increased by 19% q-o-q and 32% y-o-y to reach more than 22,150 units. Home prices rose by 2.5% during April and May, bringing a cumulative 7.4% increase for the first five months, with growth recorded across different segments.

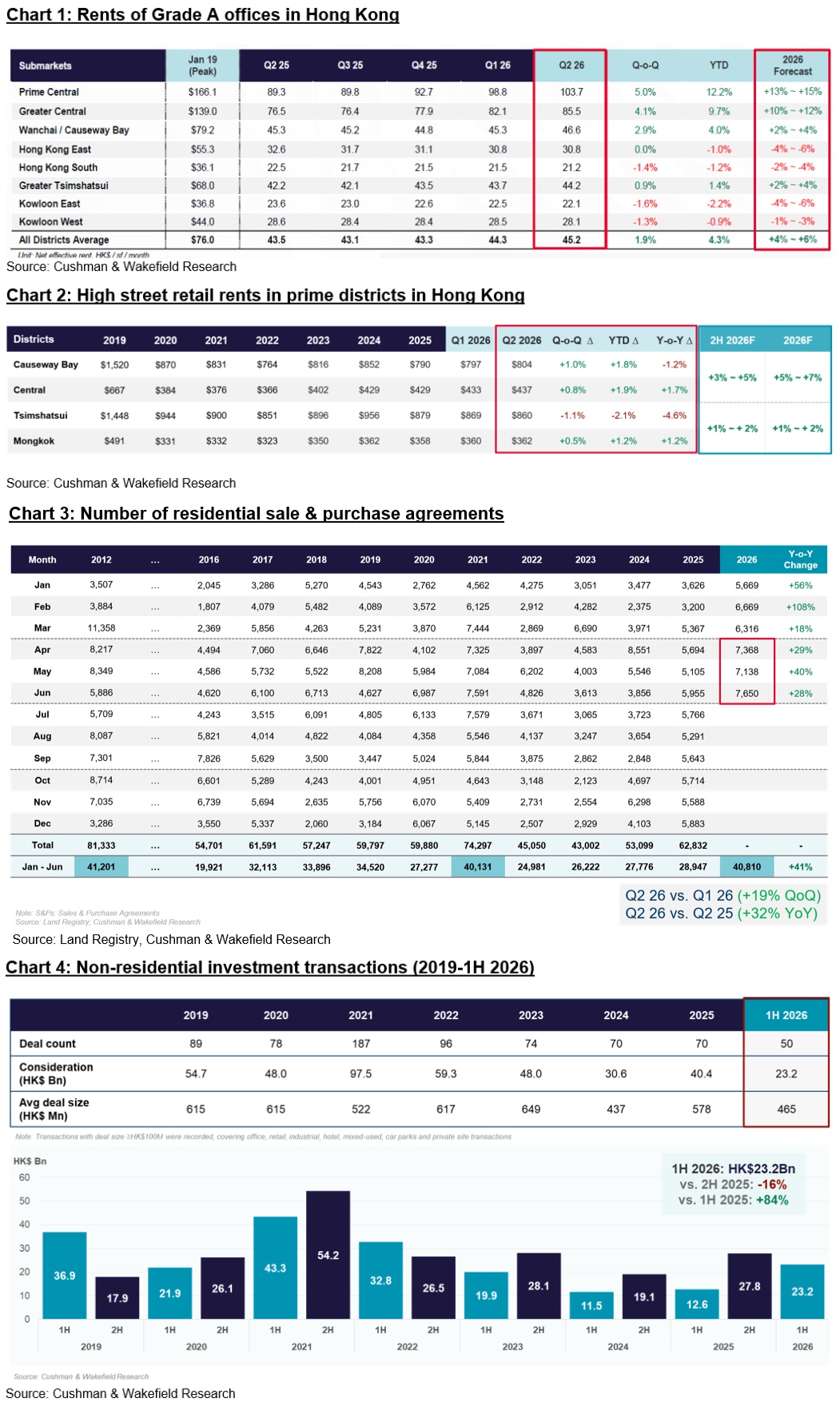

- Grade A Office Market: Citywide net absorption reached 396,100 sq ft in Q2, with new leases mainly driven by the banking & finance and insurance sectors. Core areas such as Greater Central witnessed significant rental pick up, offsetting rental corrections in non-core submarkets. Cushman & Wakefield expects the overall office market rental level to rise by +4% to +6% in 2026.

- Retail Market: Overall retail sales maintained steady growth on the back of sustained rises in inbound visitors and a stronger RMB. High street vacancy rates in Causeway Bay and Central remained at 0% in Q2, with Hong Kong Island leading a rental growth recovery.

- Capital Markets: Hong Kong’s commercial real estate investment market sustained the momentum carried over from late 2025. Supported by demand from end-users and still-attractive pricing levels across property sectors, total large-sized (>HK$100 million) non-residential transaction volume for the 1H 2026 period recorded HK$23.2 billion, up 84% y-o-y.

HONG KONG SAR – Media OutReach Newswire – 7 July 2026 – Global real estate services firm Cushman & Wakefield today held its Hong Kong Property Markets 1H 2026 Review and 2H 2026 Outlook press conference. Residential market activity remained robust as transaction numbers surpassed 22,000 cases in Q2, the highest quarterly record since Q2 2021. Grade A office market net absorption reached 396,100 sq ft in Q2, with rental level recovery mainly driven by core areas. Greater Central rents continued to pick up by 4.1% q-o-q in Q2, supporting the citywide rental level to grow by 1.9% q-o-q. In the retail sector, total retail sales continued to recover steadily, while high street store vacancy in Causeway Bay and Central returned to 0%, supporting stronger rental performance on Hong Kong Island and outpacing Kowloon. In the capital markets, end-users and well-capitalized investors bottom-fished amid attractive office asset pricing. Living sector and residential site transactions are expected to be the market focus in the upcoming months.

Grade A office leasing market: Leasing momentum driven by banking & finance and insurance sectors, rental recovery led by core areas

Driven by take-up at recent new entrants into the market, citywide office market net absorption reached 396,100 sq ft in the quarter, mainly led by Greater Central and Greater Tsimshatsui. The total new leased area reached 1.2 million sq ft in Q2, underpinned by activities from the banking & finance and insurance sectors. Rents in Greater Central continued to pick up, rising by a further 4.1% q-o-q in Q2 for total growth of 9.7% in 1H 2026, while rental level growth of 2.9% q-o-q was seen in Wanchai/ Causeway Bay. In contrast, rents in non-core areas remained soft, with all four non-core submarkets experiencing rental corrections in Q2 and 1H. The recovery in core areas has supported citywide rental growth of 1.9% q-o-q in Q2 and 4.3% for 1H 2026. In the absence of new completions in Q2, the overall availability rate fell by 0.5 percentage points q-o-q to 19.5%.

John Siu, Managing Director, Hong Kong, Cushman & Wakefield, said, “Despite the uncertainties arising from recent stock market volatility and geopolitical tensions, leasing demand from the banking & finance and insurance sectors is expected to remain resilient, backed by ongoing wealth management activities, an active IPO pipeline, and long-term operational needs from finance-related institutions. These two sectors accounted for around 60% of Grade A office new leased area in 1H 2026, compared with 38% in 2024. Following strong rental growth in Greater Central in 1H 2026, the upwards momentum is expected to moderate in 2H. Full-year rental growth in the submarket is projected in the +10% to +12% range. This will help offset the impact of rental corrections in certain non-core submarkets, and support the citywide Grade A office rental level to rise by +4% to +6% in 2026, revised upward from the previous forecast of +1% to +3%.”

Retail leasing market: High street vacancy in Causeway Bay and Central holds at 0%, more overseas brands to establish presence in Hong Kong

Sustained rises in inbound visitors, along with the wealth effect from an improving residential market and a stronger RMB, have continued to support steady growth in Hong Kong’s retail market. As at May 2026, the city’s overall retail sales marked thirteen consecutive months of y-o-y growth, while total retail sales for the January to May 2026 period recorded HK$171.5 billion, up 10.6% y-o-y. Sales growth was recorded in all key retail categories. The Jewellery & Watches sector remained the most popular among tourists, posting y-o-y growth of 26.2%, followed by the Fashion & Accessories and Medicines & Cosmetics sectors, which grew 5.4% and 5.2%, respectively.

The overall high street vacancy rate rose mildly to 5.4% in Q2 from 4.2% in Q1, chiefly driven by greater vacancies in Kowloon. Causeway Bay and Central both continued to register zero vacancies through the quarter, while vacancy rates in Tsimshatsui and Mongkok rose to 8.3% and 8.6%, respectively. Despite this, new leasing activity was witnessed across core retail districts, with relatively strong leasing demand from pharmacies and jewellery & watches retailers.

As for high street retail rents, rental recovery in Hong Kong Island continued to outperform Kowloon. Causeway Bay and Central recorded q-o-q increases of 1.0% and 0.8%, respectively, with both local and international retailers displaying preferences for these two prime high-street hubs. At the same time, the relatively affordable and reasonable rental levels in Mongkok attracted a wider range of brand entries into the district, bringing q-o-q rental growth to 0.5%. However, with the slowdown among luxury retailers, rental levels in Tsimshatsui remained under pressure, declining by 1.1% q-o-q. In the F&B sector, landlords have been more willing to offer discounts amid high availability, resulting in F&B rents across four key retail districts recording q-o-q declines within a 1% range.

John Siu commented, “Looking ahead, we expect the Hong Kong retail market to remain on a steady recovery trajectory in 2H 2026, supported by continued growth in inbound tourist numbers and recovering tourist spending amid a stronger RMB. Given still-attractive rental levels, we also expect ongoing entries of new retailers, especially from international brands who view the Hong Kong market as a strategic launchpad for regional expansion in Asia. Causeway Bay and Central are likely to remain active for leasing activities, underpinned by strong tourist footfall. We forecast high street retail rents in Causeway Bay and Central to lead a recovery and increase by 3% to 5% in 2H 2026, while we project Tsimshatsui and Mongkok to pick up modestly in the range of 1% to 2%.”

Residential market: Prices and sales rise in 1H, interest rate uncertainty may weigh on 2H sentiment

The Hong Kong residential market continued to gain momentum in Q2, with overall sentiment and transactions remaining active despite the disruptions brought on by ongoing geopolitical uncertainties. Both primary and secondary sales were strong in Q2, with the total number of residential sales and purchases agreements reaching more than 22,150 cases in the quarter, up 19% q-o-q and 32% y-o-y (Chart 3), bringing the total transaction number for the 1H 2026 period to more than 40,800 cases, a new high for the same period since 2021. As at June, the monthly number of residential sales and purchases agreements exceeded 5,000 units for 16 consecutive months, reflecting sustained buyer confidence and demand from investors. Strong sales at new launches saw primary market transactions take a 32% share of total transactions between January and May.

Edgar Lai, Senior Director, Valuation and Advisory Services, Hong Kong, Cushman & Wakefield, highlighted, “Home prices continued to increase in Q2 2026. Rating and Valuation Department data suggests that the overall residential price index picked up 2.5% in the two months from April to May, bringing 7.4% YTD growth. Meanwhile, our Cushman & Wakefield mid-and-small size units price index shows that home prices rose by 4% q-o-q and 9% in 1H. Our tracking of popular housing estates shows that price growth was witnessed across different market segments. Prices at City One Shatin, representing the mass market, rose 4.7% q-o-q, while prices at Taikoo Shing, representing the mid-market, grew by 8.6% q-o-q. Residence Bel-Air, representing the luxury segment, also recorded a notable 6.7% q-o-q rise. However, following the sustained release of pent-up demand over the past year, coupled with rising stock market volatility in June and tighter cross-border capital controls from the Chinese mainland, our June Verbal Enquiry index indicates that buyer enquiries moderated towards the end of the quarter, compared with the peak seen in April and May.”

Rosanna Tang, Deputy Managing Director, Head of Research, Hong Kong, Cushman & Wakefield, added, “The Hong Kong residential market extended its positive momentum in Q2, with overall transaction activity remaining vibrant. Total residential transaction numbers in the quarter exceeded 22,150 cases, marking a new high since Q2 2021. Looking ahead to 2H, uncertainties in interest rate movements are expected to widen. Some potential buyers may again observe how geopolitical developments and stock market trends are affecting capital flow and market sentiment. Yet, given the resilient housing demand in the city, backed by rising numbers from incoming talent and non-local students, Hong Kong residential market is expected to remain stable in 2H. We anticipate full-year transactions in 2026 to reach approximately 75,000 units, while home prices to pick up by close to 10%. In terms of rents, rental index picked up by 1.8% in the first five months in 2026, rising 18% from the last bottom in 2023. Rental growth is expected to be moderate and stay within 5% y-o-y in 2026.”

Non-residential investment market (dealsexceeding HK$100 million): Transaction momentum sustains, with end-users leading office transactions

Amid the still-attractive pricing across property sectors, the Hong Kong commercial real estate investment market largely sustained the transaction momentum carried over from 2H 2025. The city’s non-residential investment market for deals exceeding HK$100 million recorded 50 transactions in 1H 2026, with total transaction volume rising 84% y-o-y to HK$23.2 billion, although down 16% from the HK$27.8 billion seen in the 2H 2025 period. (Chart 4). In 1H 2026, local buyers remained the major source of capital, accounting for more than 70% of the total consideration. Foreign capital comprised 19% of 1H 2026 total transaction volume, drawn by discounted property prices and conversion projects with value-added angles. By asset class, the office sector accounted for 54% of total investment consideration, followed by around 23% from the hotel / rental housing sector.

Tom Ko, Executive Director and Head of Capital Markets, Hong Kong, Cushman & Wakefield, concluded, “In 1H 2026, office sales transactions continued to account for the largest share of both consideration and deal count, indicating a recovery in the investment ecosystem. During this round of consolidation, end-user buyers acted to capture bottom-fishing opportunities, with multiple large-scale office deals concluded. Our recent publication in May 2026, Hong Kong Office Building Investment Back in Focus: A Market Reassessment, suggests the significant capital value adjustment has reset entry levels and reopened the market to end-users seeking bottom-fishing opportunities, especially for education institutions, banks and financial institutions, as well as leading Chinese mainland corporates.

“Notably, some end-user buyers are cash-rich and therefore less sensitive to banks’ cautious lending stance toward commercial properties, and to interest rate movements. Office capital values are projected to follow the recovery in rents. Coupled with the declining availability of distressed office assets, the current market encourages end-users to accelerate their decision-making to consider bottom-fishing ahead of the subsequent upcycle. Looking ahead to 2H 2026, we believe demand from end-users and the living sector will remain the major drivers of investment activity. The market has also witnessed growing momentum in private residential sites transactions, with investors strategically expanding land banks amid a buoyant residential market. We expect to see more transactions in this segment through the remainder of the year. Against this backdrop, the 2026 full-year investment volume is now forecast to reach more than HK$40 billion.”

Please click here to download photo and presentation deck.

(From left to right) Tom Ko, Executive Director and Head of Capital Markets, Hong Kong, Cushman & Wakefield; John Siu, Managing Director, Hong Kong, Cushman & Wakefield; Rosanna Tang, Deputy Managing Director, Head of Research, Hong Kong, Cushman & Wakefield and Edgar Lai, Senior Director, Valuation and Advisory Services, Hong Kong, Cushman & Wakefield.

Hashtag: #Cushman&Wakefield

The issuer is solely responsible for the content of this announcement.

Cushman & Wakefield (NYSE: CWK) is a leading global commercial real estate services firm for property owners and occupiers with approximately 53,000 employees in nearly 350 offices and 60 countries. In Greater China, a network of 23 offices serves local m

Cushman & Wakefield (NYSE: CWK) is a leading global commercial real estate services firm for property owners and occupiers with approximately 53,000 employees in nearly 350 offices and 60 countries. In Greater China, a network of 23 offices serves local markets across the region. In 2025, the firm reported revenue of $10.3 billion across its core services of Valuation, Consulting, Project & Development Services, Capital Markets, Project & Occupier Services, Industrial & Logistics, Retail, and others. Built around the belief that Better never settles, the firm receives numerous industry and business accolades for its award-winning culture. For additional information, visit www.cushmanwakefield.com.hk or follow us on LinkedIn (https://www.linkedin.com/company/cushman-&-wakefield-greater-china).